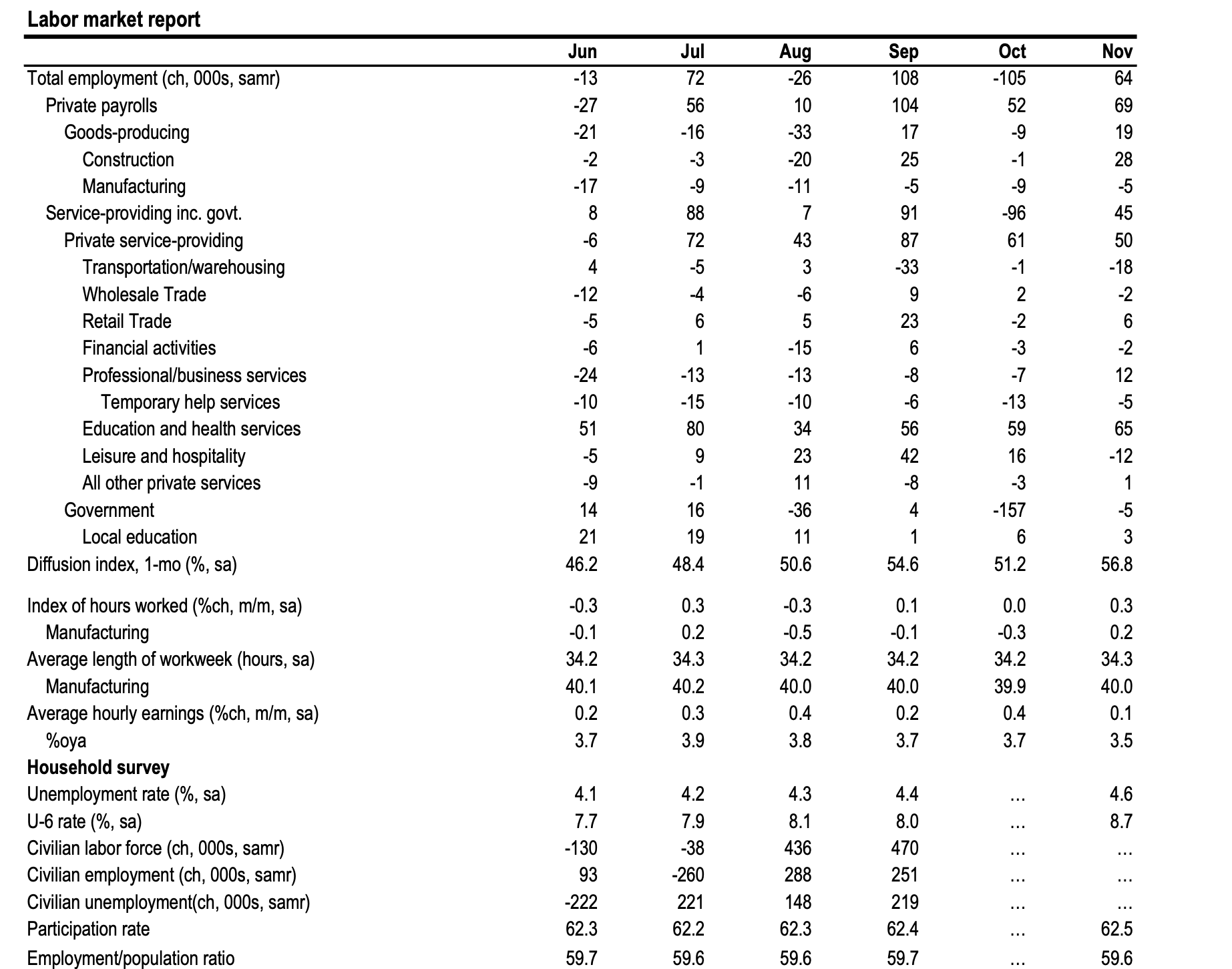

The simultaneous release of the November and partial October employment reports could have been a source of significant volatility, but the data ultimately failed to shift the labor market narrative established prior to the government shutdown. Private payrolls grew by 52,000 in October and 69,000 in November, hovering remarkably close to the three- and six-month averages through September. While the headline unemployment rate climbed from 4.4% to 4.6% during this two-month gap, our analysis suggests that after adjusting for technical distortions, the real increase was marginal. This remains consistent with the established trend of a slow, gradual cooling in the labor market. Critical establishment survey metrics—specifically an average workweek fluctuating between 34.2 and 34.3 hours and monthly wage growth averaging 0.3%—remained insulated from the “job count” doubts raised by Chair Powell. These figures signal no abrupt collapse in business labor demand, even as the household survey warrants a more skeptical, albeit cautious, reading. We maintain our conviction that these signs of slack will prompt the Fed to deliver one final rate cut in January, contingent on the cleaner December print confirming this trajectory. Concurrently, we anticipate a downshift in annualized GDP growth to 1.0% this quarter, weighed down by dampened consumer spending and shutdown-related frictions.

Within the establishment survey details, the October headline of -105,000 was severely distorted by 162,000 DOGE-related deferred resignations, with federal payrolls shedding another 5,000 in November. The private sector saw goods-producing roles dip by 9,000 in October before a 19,000-job recovery in November, almost entirely construction-led. Conversely, manufacturing remains a clear laggard, contracting for seven consecutive months. A more concerning structural development is that healthcare and social assistance accounted for the entirety of private job growth over the last two months, with cyclically sensitive service industries remaining flat. While average hourly earnings rose 0.44% in October and a more subdued 0.14% in November, the year-over-year figure hit a cycle low of 3.5%. Interestingly, the measure for production and non-supervisory workers proved more resilient at 3.9%. Despite the reporting delays, survey collection rates were surprisingly high, providing some baseline confidence in these establishment figures.

The household survey, however, requires a much heavier discount. The unemployment rate’s rise from 4.44% to 4.56% includes a roughly 4bp “statistical phantom” caused by rotation group bias from the skipped October survey. Adjusting for this, the 4bp monthly increase since September aligns almost perfectly with the 3bp monthly trend seen over the past year. Given the elevated standard errors, a definitive assessment of labor market slack is impossible until we see the December data. Participation remained stagnant at 62.5%, while the employment ratio matched its recent low of 59.6%. The internal details offered a mix of “fuzzy” signals: the September surge in permanent job losers reversed, and recent unemployment was largely driven by labor market reentrants—both positive developments. However, the U-6 underutilization rate’s jump from 8.0% to 8.7% cannot be ignored. Since U-6 is less sensitive to rotation bias than U-3, it suggests genuine underlying softening. For now, the household survey should be treated with healthy skepticism as we await a cleaner read.