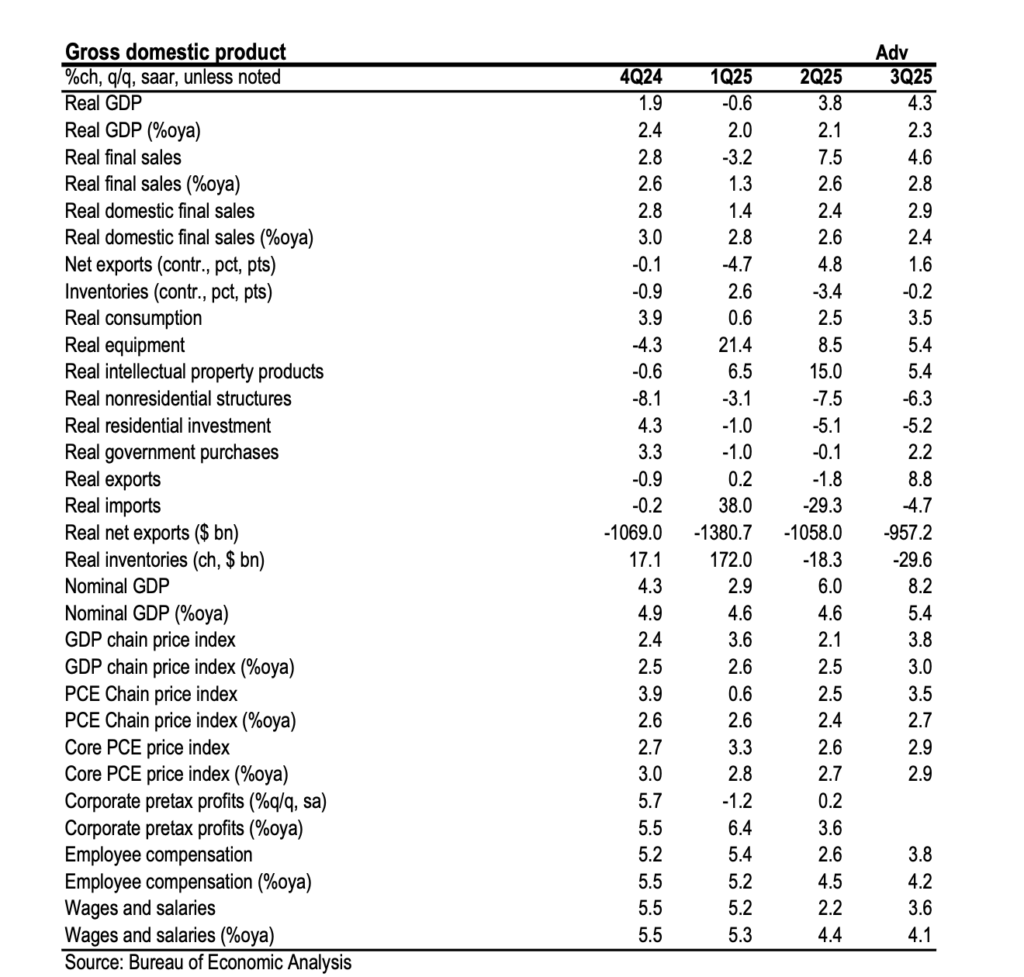

• Real GDP rose 4.3%q/q, saar in 3Q, the strongest increase in two years

• Strong growth reflected a pickup in consumer spending as well as robust capex and government spending on defense

• Core PCE inflation rose 2.9%q/q, saar; the GDP price index jumped 3.8%

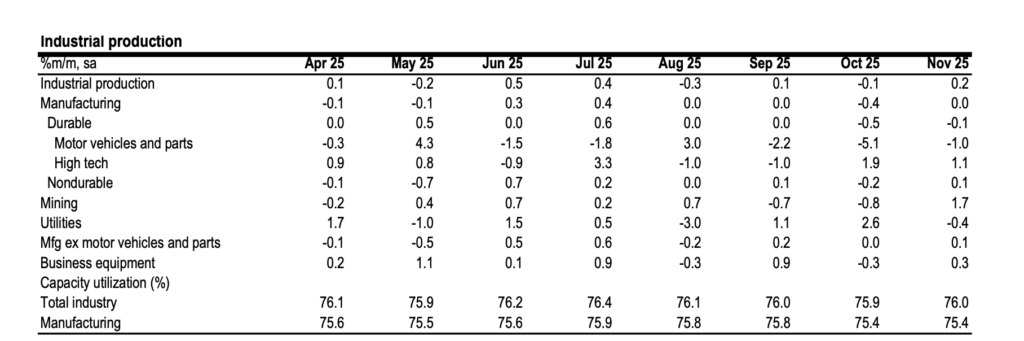

• October-November IP data show growth in manufacturing moderating

• Further deterioration in Conference Board consumer confidence accompanied by weaker labor market differential

Real GDP surged at a 4.3% annualized rate in the third quarter, delivering the strongest quarterly expansion in two years and handily beating both the consensus and our own upgraded 3.5% forecast. This print confirms significant mid-year momentum, effectively brushing off concerns regarding a softening labor market. While growth has averaged 2.5% across 2025, we now see meaningful upside risk to our 1.0% projection for the fourth quarter. The primary engine was a 3.5% acceleration in consumer spending, with robust demand spanning both goods and services. Business investment remained durable at 2.8%, despite a sharper-than-expected 6.3% contraction in non-residential structures. However, equipment spending surprised to the upside at 5.4%, bolstered by tech imports that suggest continued strength through year-end. Government spending and net exports also provided tailwinds, though a 3.8% jump in the GDP price index—despite core PCE printing in line at 2.9%—highlights persistent inflationary heat.

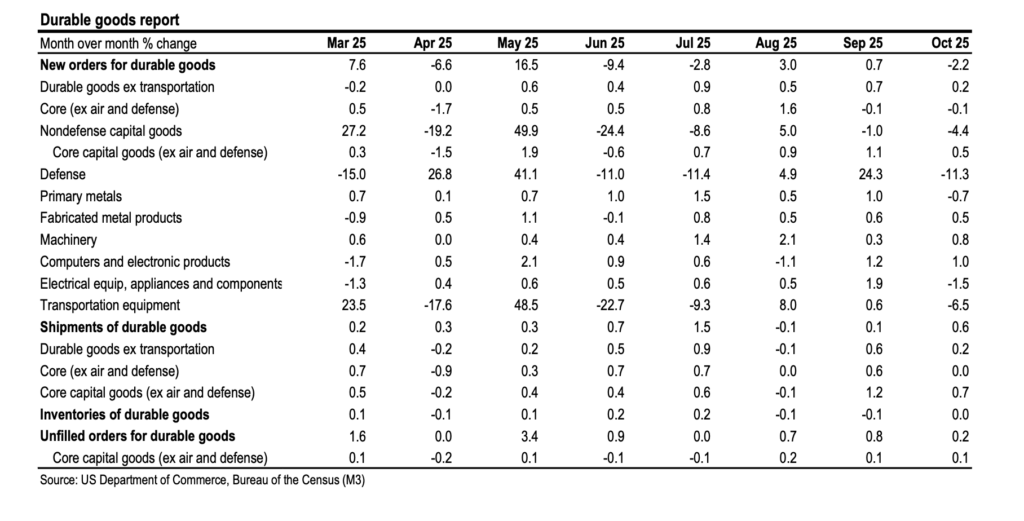

Due to the government shutdown, this report serves as a consolidated look at both GDP and GDI, the latter of which rose a more modest 2.4%. Corporate health remains a bright spot; pre-tax profits jumped 4.2% in Q3—a 9.1% year-over-year increase—proving that firms are successfully navigating rising tariff costs. Looking ahead, we anticipate a consumption slowdown as policy headwinds mount and higher tariffs firm up inflation. That said, technical measurement issues may temporarily inflate Q4 real household spending data. While October’s durable goods orders fell 2.2% headline, this was largely a defense-driven drag. The core capital goods segment—nondefense ex-aircraft—remains on a steady uptrend, with orders and shipments rising 0.5% and 0.7%, respectively. We are fading the weakness in manufacturing surveys, expecting tech imports and a recovery in the motor vehicle and aircraft sectors to bridge the gap into 2026.

Industrial production data arrived with a softer tilt, showing a combined stagnation across October and November. Manufacturing IP contracted 0.4% in October before a tepid 0.1% recovery in November, largely due to volatility in motor vehicles. However, aircraft manufacturing remains a powerhouse, growing 3.2% cumulatively as it moves past last year’s strike disruptions, while computer equipment IP surged 2.5% in November. The most significant red flag comes from the Conference Board’s December Consumer Confidence report, which tumbled to 89.1. The “present situation” index hit a five-year low, and the labor market differential collapsed to 5.9%—levels not seen since early 2021. This deterioration in sentiment strongly suggests a further rise in the unemployment rate, prompting us to lift our peak unemployment forecast to 4.7% for the first quarter of 2026.