The FOMC delivered a widely anticipated 25bp cut today, lowering the target range to 3.5–3.75%. The meeting featured a three-way split in dissents—two hawkish and one dovish—perfectly mirroring consensus expectations. While the “dot plot” remained largely unchanged from September, the overarching message from the statement and Chair Powell’s press conference was clear: the era of “risk management” cuts is likely over. With policy rates now perceived to be within the plausible range of neutral—a term Powell highlighted a dozen times—the Fed has signaled that further accommodation will require a “material deterioration” in labor data. Powell remains notably relaxed regarding inflation, viewing current levels as no barrier to a hold, provided the labor market doesn’t fracture. We maintain our call for one final cut next month, but we acknowledge this is now entirely data-dependent and contingent on the December jobs report showing genuine slack.

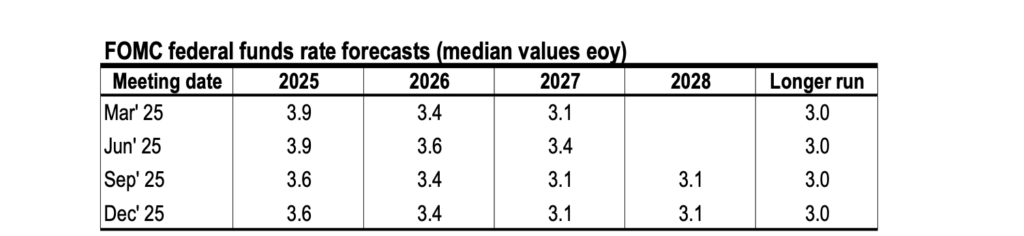

The shift in forward guidance was subtle but significant, utilizing the “Fedspeak” signal of adding “the extent and timing” to describe future cuts. Historically, this phrase serves as a precursor to an extended pause, much like the pivot witnessed last December. In another descriptive tweak, the Committee dropped the characterization of the unemployment rate as “low,” a dovish acknowledgement of recent softening that was ultimately overshadowed by the hawkish guidance shift. Dissents from Miran (50bp) and Schmid (hold) were expected, though Goolsbee’s move to join the hawks for a hold provided a modest surprise. The median dots still project only one cut in 2026 and another in 2027, with six participants already signaling they would have preferred no action today. Crucially, despite Powell’s “neutral” rhetoric, the median long-run dot remains anchored at 3.0%, suggesting the Committee still views current levels as restrictive rather than balanced.

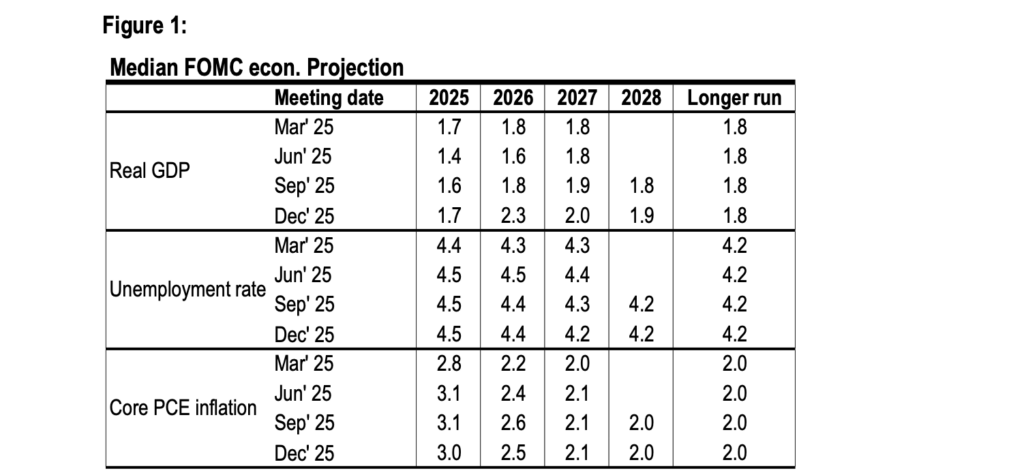

Economic forecasts saw GDP growth for next year marked up by 50bp, partially attributed to the technical unwind of the government shutdown and an “AI capex effect,” while 2026 inflation was revised down by a tenth. Powell’s rhetoric suggested the Fed believes it has done “enough for now,” stating the current stance is “well positioned” to let inflation resume its downward trend once tariff effects pass. Interestingly, Powell raised eyebrows by suggesting job growth remains overstated by roughly 60,000 per month, implying that underlying private-sector hiring may already be negative. In a tactical move, the Committee initiated $40 billion in monthly reserve management purchases (RMP) of bills to navigate April tax season liquidity, while simultaneously shifting standing repo operations to a full allotment format. This combination suggests a Fed that is confident in its current rate path but remains hyper-vigilant regarding back-end plumbing and labor market tail risks.